Long Term Commercial Loans – Best Business Financing Options for Growth in 2026

Long Term Commercial Loans : Why Smart Businesses Borrow Slowly Instead of Desperately

A lot of business owners wait too long to think about financing.

Sales dip for 3 months. Equipment starts failing. Payroll pressure builds. Then panic enters the room and suddenly they’re applying for expensive short-term loans at ugly interest rates.

That pattern repeats constantly in the U.S.

The businesses that usually survive longer plan financing before things get messy.

And that’s where long term commercial loans come in.

These loans give businesses access to larger amounts of capital with repayment periods that often stretch from 5 to 25 years depending on the loan type.

Lower monthly payments. Longer breathing room. Bigger projects.

Still, long-term debt can help a business grow or quietly choke its cash flow for years. Depends how the owner uses it.

What are Long Term Commercial Loans?

Long Term Commercial Loans are business repaid over several years instead of a few months.

Businesses often use them for:

- Real estate purchases

- Expansion projects

- Equipment financing

- Renovations

- Inventory growth

- Franchise development

- Refinancing debt

Long terms commonly range between:

- 5 years

- 10 years

- 20 years

- 25 years

Commercial real estate loans sometimes go even longer.

The bigger the project, the more likely long repayment periods become necessary.

A restaurant owner buying ovens probably doesn’t need 20 years.

Someone purchasing a $2 million warehouse probably does.

Why Businesses Choose Long-Term Financing

Cash flow.

That’s the entire conversation most of the time.

A shorter loan may technically save interest overall, but the monthly payments can become brutal.

Example:

- $300,000 repaid over 3 years creates heavy monthly obligations

- The same amount spread across 15 years becomes more manageable

Businesses care deeply about monthly cash survival because payroll, rent, taxes, utilities, insurance, and supplier costs never stop.

A business can look profitable on paper while dying from cash flow pressure.

That happens constantly.

Common Types of Long Term Commercial Loans

Several financing products fall into this category.

Each works differently.

Traditional Bank Term Loans

Banks still handle large portions of commercial lending in the U.S.

These loans usually work best for businesses with:

- Strong credit

- Consistent revenue

- Established operating history

- Healthy cash reserves

Banks prefer stability.

A business showing 5 years profitable tax returns gets treated very differently than a startup operating from a laptop and caffeine.

Typical repayment terms:

- 5 to 10 years

- Sometimes longer for major projects

SBA Loans

The U.S. Small Business Administration backs several business laon programs

SBA loans became extremely popular because often provide:

- Lower down payments

- Longer repayment periods

- Competitive interest rates

The SBA doesn’t directly lend most money itself.

Banks and approved lenders usually issue the loans while SBA guarantees reduce lender risk.

SBA 7(a) Loans

These Loans often fund:

- Working capital

- Equipment

- Expansion

- Real estate

- Refinancing

Terms may stretch up to:

- 10 years for working capital

- 25 years for commercial real estate

SBA 504 Loans

These loans focus heavily on:

- Commercial property

- Major equipment purchases

Manufacturing companies and growing businesses use them frequently.

Long Term Commercial Loan Types Comparison

| Loan Type | Typical Loan Amount | Repayment Term | Best For | Collateral Required |

| Traditional Bank Term Loan | $50,000 – $5 Million + | 5-10 Years | Established Businesses | Usually Yes |

| SBA 7(a) Loan | Up to $5 Million | Up to 25 Years | Expansion & Working Capital | Often Required |

| SBA 504 Loan | Up to $5.5 Million + | 10-25 Years | Commercial Real Estate & Equipment | Yes |

| Commercial Real Estate Loan | $1,00,000-$20 Million + | 10-25 Years | Property Purchases | Property Secures Loan |

| Equipment Financing | $10,000 – $10 Million + | 3-15 Years | Machinery & Equipment | Equipment Secures Loan |

| Franchise Financing | Varies by Franchise | 5-25 Years | Franchise Development | Often Required |

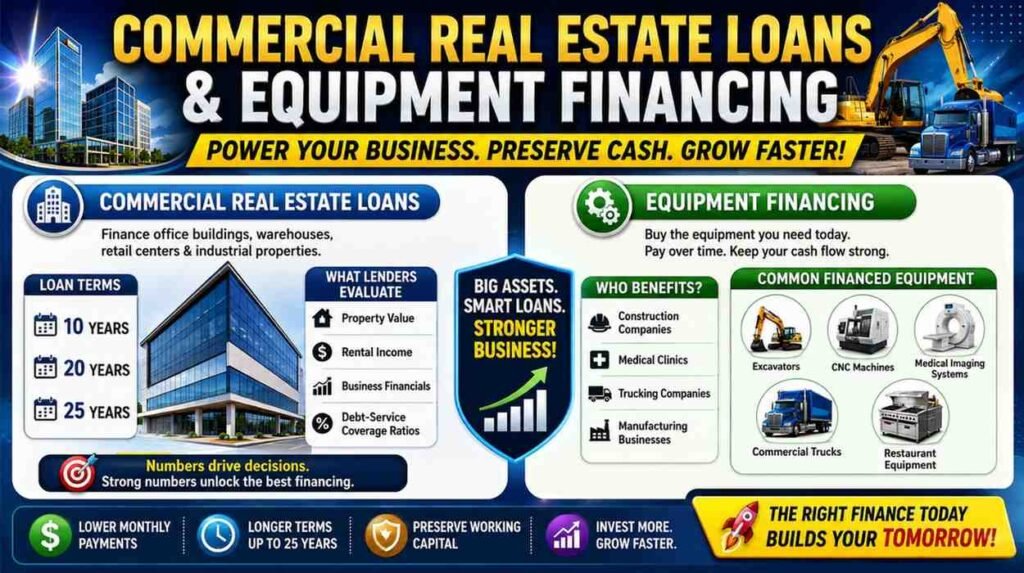

Commercial Real Estate Loans

Businesses buying office buildings, warehouses, retail centers, or industrial property often use commercial real estate financing.

These loans may run:

- 10 years

- 20 years

- 25 years

Lenders examine:

- Property value

- Rental income

- Business financials

- Debt-service coverage ratios

Commercial real estate lending becomes heavily numbers-driven fast.

Equipment Financing

Large equipment purchases can destroy cash reserves if paid upfront.

Construction companies, medical clinics, trucking firms, and manufacturing businesses often finance equipment over longer periods.

Common Financed Equipment:

- Excavators

- CNC machines

- Medical imaging systems

- Commercial trucks

- Restaurant equipment

One MRI machine alone can cost more than several houses in some states.

Franchise Financing

Franchise businesses often use long-term commercial loans because startup costs can get massive quickly.

Common expenses include:

- Franchise fees

- Equipment

- Build-outs

- Inventory

- Commercial leases

Popular franchise sector include:

- Fast food

- Fitness centers

- Hotels

- Auto services

And some franchise owners underestimate startup costs badly.

The opening-week excitement disappears fast when HVAC repairs arrive.

How Lenders Decide Whether to Approve a Business

Lenders study risk constantly

The care about one main question:

‘Will this business reliably repay the loan’?

Everything eslse supports that question.

Credit Score

Business owners with stronger personal credit generally receive better loan terms.

Especially for smaller businesses.

A poor credit score doesn’t always kill approval chances, but it often increases rates or collateral requirements.

Revenue and Cash Flow

Lenders want proof the business generates stable income.

Many lenders request:

- Tax returns

- Bank statements

- Profit-and-loss statements

- Balance sheets

Cash flow matters heavily because monthly payments must fit inside real operating numbers.

Time in Business

Older businesses usually qualify more easily.

A company operating profitably for 8 years looks safer than a startup launched 6 months ago.

Startups often face:

- Higher rates

- Smaller approvals

- More collateral demands

Collateral

Large long-term commercial loans frequently require collateral.

Collateral may include:

- Real estate

- Equipment

- Vehicles

- Inventory

If the business defaults, the lender may seize pledged assets.

That part becomes very real during economic downturns.

Debt-Service Coverage Ratio

Commercial lenders analyze whether business income comfortably covers debt payments.

If a business barely survives month to month already, lenders become cautious fast.

A lender reviewing numbers wants breathing room, not desperation.

Interest Rates on Long Term Commercial Loans

Rates vary heavily depending on:

- Credit quality

- Loan type

- Market conditions

- Business strength

- Collateral

- Loan size

SBA loans often carry lower rates than unsecured online business loans.

Riskier businesses usually pay more.

And variable-rate loans create extra uncertainty because future payments can rise if interest rates incerase.

A business owner borrowing during low-rate periods may feel shocked during refinancing later if rates jump several percentage points.

Fixed vs Variable Interest Rates

Both structures appear often in commercial leding.

Fixed-Rate Loans

The interest rate stays cosistent.

Benefits include:

- Predictable monthly payments

- Easier budgeting

- Less interest-rate risk

Many businesses prefer fixed rates for stability.

Variable-Rate Loans

Rates fluctuate based on market indexes.

These loans sometimes begin with lower initial rates.

But payments can rise later.

That risk matters more during volatile economic periods.

Best Uses for Long-Term Commercial Loans

Some investments justify long-term debt well.

Others don’t.

Buying Commercial Property

Owning property can stabilize long-term operating costs.

Instead of paying rising rent forever, businesses build equity over time.

Many businesses eventually view commercial property ownership as a major financial turning point.

Expanding Operations

Growing businesses often need:

- Larger facilities

- More staff

- Better equipment

- Additional inventory

Long-term financing helps spread expansion costs across years rather than crushing monthly cash flow immediately.

Refinancing Expensive Debt

Some businesses refinance short-term debt into longer repayment structures.

This can lower montlhy payment pressure.

Still, refinancing bad business habits rarely fixes deeper operational problems.

A struggling business with weak sales doesn’t magically recover because debt lasts longer.

Purchasing Expensive Equipment

Heavy machinery, medical systems, or industrial equipment often generate revenue for many years.

Long repayment periods match the equipment’s working lifespan better.

Risks of Long Term Commercial Loans

Long repayment periods sound comfortable until business conditions change.

And business conditions always change eventually.

Total Interest Costs Rise

Longer Terms reduce monthly payments while increasing total interest paid over time.

That trade-off matters.

Borrowing $500,000 over 20 years can produce massive total repayment amounts.

Economic Downturns Happen

Businesses borrowing during strong markets sometimes struggle later during recessions.

Consumer spending falls. Revenue tightens. Debt payments remain.

Loan obligations don’t care about bad quarters.

Personal Guarantees Create Risk

Many lenders require business owners to personally guarantee loans.

That means personal assets may become vulnerable if the business fails.

Some owners underestimate how serious personal guarantees actually are.

Overexpansion Hurts Businesses Constantly

Easy financing tempts businesses into oversized expansion plans.

Extra locations, bigger payroll, expensive renovations, unnecessary equipment.

Growth funded poorly can wreck healthy businesses surprisingly fast.

Long Term Commercial Loan Qualification Requirements

| Approval Factor | What Lenders Look For | Why It Matters |

| Credit Score | Typically 680+ Preferred | Lower Risk Borrowers Receive Better Terms |

| Annual Revenue | Stable & Consistent Revenue Growth | Demonstrates Repayment Ability |

| Time in Business | Usually 2 + Years Preferred | Shows Business Stability |

| Cash Flow | Positive Monthly Cash Flow | Supports Ongoing Loan Payments |

| Collateral | Property, Equipment, Inventory, Vehicles | Reduces Lender Risk |

| Debt-Service Coverage Ratio (DSCR) | Usually 1.25 or Higher | Indicates Ability to Cover Debt |

| Business Plan | Strong Growth Strategy | Important for Larger Loans |

| Industry Experience | Relevant Industry Knowledge | Improves Lender Confidence |

Best-Known Lenders for Long Term Commercial Loans

Several lenders dominate commercial financing conversations in the United States.

Common Lenders Include:

- Bank of America Business Lending

- Wells Fargo Business Lending

- Chase Business Banking

- Live Oak Bank

- U.S. Small Business Admiistration

Approval standards vary heavily between lenders.

Some banks prefer large established businesses. Others actively target smaller companies and SBA lending.

Online Lenders vs Traditional Banks

Online business lenders grew fast because traditional bank approval can feel painfully slow.

Banks may take weeks or months reviewing applications.

Online lenders sometimes move within days.

Still, faster oney often comes with:

- Higher interest rates

- Shorter terms

- More aggressive repayment structures

Speed gets expensive in lending.

Usually very expensive.

Documents Businesses Usually Need

Commercial loan applications often require:

- Business tax returns

- Personal tax returns

- Profit-and-loss statements

- Bank statements

- Business licenses

- Financial projections

- Balance sheets

- Debt schedules

Commercial ending paperwork stacks up fast.

Especially for larger loans.

How Businesses Improve Approval Odds

Several things help businesses qualify more easily.

Improve Bookkeeping

Messy financial records scare lenders.

Clear accounting matters heavily.

Reduce Unnecessary Debt

Heavy debt loads weaken approval strength.

Increase Cash Reserves

Lenders like businesses with financial cushions.

Emergency reserves reduce perceived risk.

Build Business Credit

Healthy business credit profiles improve financing opportunities over time.

Show Stable Revenue Trends

Consistent growth matters more than random spikes.

Lenders prefer predictable businesses over chaotic ones.

Common Mistakes Businesses make with Long-Term Loans

Business owners repeat similar financing mistakes constantly.

Borrowing Too Much

Extra money feels comforting initially.

Large monthly obligations feel much less comforting later.

Ignoring Total Repayment Cost

People focus heavily on monthly payments and ignore total long-term cost.

That math matters.

Expanding Too Fast

Second locations destroy businesses every year.

Especially restaurants.

A profitable first location doesn’t guarantee success elsewhere.

Using Long-Term Debt for Short-Term Problems

Long-term financing works best for long-term assets and projects.

Using 15-year financing to temporarily patch weak sales creates future problems.

Final Thoughts on Long Term Commercial Loans

Long-term commercial loans can help businesses grow responsibly when owners plan carefully and borrow realistically.

They also create long-term pressure that follows businesses for years.

The smartest borrowers usually:

- Understand total repayment costs

- Protect cash flow carefully

- Avoid oversized expansion

- Compare multiple lenders

- Read loan agreements slowly

- Borrow with realistic revenue expectations

And one thing matters more than flashy growth plans:

Stable cash flow.

A boring profitable business with manageable debt usually survives longer than an aggressive business trying to look bigger than it actually is.

FAQs (Long Term Commercial Loans)

- What is the Longest term for a commercial loan?

The longest commercial loan terms typically range from 20 to 25 years, especially for commercial real estate financing and SBA backed loans. Some specialized property loans may extend beyond 25 years depending on the lender, property type, and borrower qualifications. - What are the 4 types of commercial banks?

The four common types of commercial banks in the United States are:

A) Retail Banks

B) Business (Commerical) Banks

C) Investment Banks

D) Universal Banks

Each serves different financial needs, from personal banking to large scale business lending and investment services. - What is the TLA and TLB in commercial lending?

A) TLA : Typically offered by banks, features shorter repayment periods and regular amortization.

B) TLB : Usually provided by institutional lenders, offers longer terms with lower periodic principal payments and a larger balloon payment at maturity.

Large corporations often use TLB financing for aquisitions and expansion projects. - What is a long term loan for a business?

A long term business loan is financing that is repaid over several years, typically 5 to 25 years. Businesses use long term loans for real estate purchases, expansion projects, equipment acquisitions, refinancing, and other major investments that generate long term value. - What credit score is needed for a commercial loan?

Most traditional lenders prefer a personal credit score 680 or higher. SBA lenders may approve some borrowers with lower scores, but stronger credit generally results in better interest rates and loan terms. - Can startups qualify for long term commercial loans?

Yes, but qualification can be more challenging. Startups often need strong personal credit, a detailed business plan, sufficient collateral, and evidence of projected revenue to secure long term financing. - Are SBA loans considered long term commercial loans?

Yes. SBA 7(a) and SBA 504 loans are among the most popular long term commercial financing options in the United States. Repayment terms can extend up to 25 years, depending on the loan purpose. - What can a long term commercial loan be used for?

Businesses commonly use long term commercial loans for:

A) Commercial Real Estate Purchases

B) Equipment Financing

C) Business Expansion

D) Franchise Development

E) Debt Refinancing

F) Facility Renovations

G) Inventory Growth - What is the difference between a commercial loan and a business loan?

A business loan is a broad category covering all types of business financing. A commercial loan usually refers to larger financing used for income producing activities such as commercial property purchases, expansion projects, or major equipment investments. - How long does it take to get approved for a commercial loan?

Approval timelines vary by lender. Traditional banks may take several weeks to several months, while online lenders can sometimes provide decisions within a few business days. SBA loans typically require more documentation and often take longer to process

Sources & References:-

- U.S. Small Business Administration (SBA) – Loan Programs

2. SBA 7(a) Loan Program Guide

3. SBA 504 Loan Program Guide

4. Federal Reserve – Small Business Credit Survey

5. Consumer Financial Protection Bureau (CFPB) – Small Business Lending Resources

6. Bank of America Business Lending

7. Wells Fargo Business Financing

8. JPMorgan Chase Business Banking & Lending

9. Live Oak Bank Commercial & SBA Lending

10. Investopedia – Commercial Real Estate Loans Guide

Article was Last Updated on 25th June 2026

For More Updates Please Follow Click Here