Business Insurance Kansas – Complete Small Business Coverage Guide

Running a business in Kansas sounds simple until something wrong

A customer slips inside your store

A company truck gets into a accident

A tornado damages your office roof

An employee gets injured lifting equipment

A lawsuit arrives unexpectedly on a random Tuesday afternoon and suddenly your peaceful coffee tastes like financial panic

That’s why business insurance matters

A lot

Kansas businesses deal with real risks every year, especially because the state has strong agriculture, transportation, construction, manufacturing, and small business activity spread across both cities and rural areas.

And unlike internet business advice pretending every company runs from a beach laptop real businesses carry real risk

Insurance helps absorb financial damage before it destroys everything you built

Why Business Insurance Matters in Kansas

Kansas has over 300000 small businesses

That includes:

- Restaurants

- Farms

- Retail stores

- Contractors

- Trucking companies

- Medical offices

- Local service businesses

Each one faces different risks

A construction company inn Wichita doesn’t face the same exposure as a bakery in Topeka or a trucking operation moving freight across interstate 70 during brutal winter weather.

Still, every business shares one thing:

Problems get expensive fast.

One lawsuit alone can wipe out years of profits for an uninsured company

What Business Insurance Actually Covers

Business insurance is basically financial protection for company related losses

Different policies cover different situations

Common protections include:

- Property damage

- Lawsuits

- Employee injuries

- Vehicle accidents

- Theft

- Storm damage

- Legal costs

Many Kansas business owners buy multiple policies bundled together because single policies rarely cover everything

And yes, insurance paperwork feels overwhelming initially

The wording sometimes sounds like it was written by lawyers competing in a national ‘least understandable sentence’ tournament.

Types of Business Insurance in Kansas

Different businessses need different protection

Still, certain policies appear repeatedly across industries

General Liability Insurance

This is one of the most common policies for Kansas businesses

General liability insurance usually covers:

- Customer injuries

- Property damage claims

- Legal defense costs

- Advertising-related claims

Example:

A customer slips on wet flooring inside your coffee shop and breaks an ankle

Medical bills arrive

Legal threats appear

Insurance potentially helps cover costs

Without coverage, small businesses often pay out-of-pocket

That becomes brutal financially

Commercial Property Insurance

Kansas weather creates serious property risks

Storms

Hail

Wind damage

Tornadoes

Commercial property insurance helps cover buildings, inventory, furniture and equipment damaged by covered events

A retail shop losing inventory after storm damage could face massive losses otherwise

Especially smaller companies without huge emergency reserves.

Workers Compensation Insurance

Kansas law generally requires workers compensation coverage for businesses with employees

This insurance helps cover:

- Medical expenses

- Lost wages

- Workplace injury claims

Construction, manufacturing, and agriculture businesses especially need strong coverage because injury risks stay higher.

Back injuries alone create huge claims regularly

Humans apparently keep discovering creative new ways to injure themselves while lifting thing incorrectly.

Commercial Auto Insurance

A personal car policy usually won’t fully protect business vehicles

That surprises some owners badly

Commercial auto insurance helps businesses using:

- Delivery vans

- Trucks

- Service vehicles

- Company cars

Kansas businesses with transportation exposure face major accident risk because employees spend long hours on roads statewide

One serious collision can become financially devastating without proper coverage.

Professional Liability Insurance

This matters for service-based businesses

Accountants

Consultants

Real Estate Professionals

Marketing Agencies

Financial Advisors

Professional liability insurance helps cover claims involving mistakes, negligence, or professional errors.

Clients sue businesses for financial losses more often than many owners expect

Especially when money gets involved.

Cyber Insurance

Cyberattacks hit small businesses constantly now.

Hackers don’t only target giant corporations

Smaller businesses often have weaker security systems, making them easier targets.

Cyber insurance may help cover:

- Data Breaches

- Ransomware Attacks

- Customer Notification Costs

- Recovery Expenses

And yes, ransomware attacks on small businesses became frighteningly common across the United States.

Some owners still think cybersecurity only matters for Silicon Valley Tech Companies.

Then one phishing email detonates inside the office network like digital fireworks fueled by regret.

Business Owner’s Policy (BOP)

Many Kansas small businesses buy BOP coverage

This Combines:

- General Liability

- Commercial Property Insurance

Bundling policies often lowers costs compared to buying everything seperately

Restaurants, retail stores, and offices commonly use BOP structures.

How Much Business Insurance Costs in Kansas

Pricing depends heavily on business type

A small phogoraphy studio won’t pay what a roofing company pays

That would make zero sense

Here’s rough idea:

| Business Type | Estimated Monthly Cost |

| Small Office Business | $40 to $100 |

| Retail Store | $60 to $200 |

| Restaurant | $120 to $400 |

| Contractor Business | $150 to $600+ |

| Trucking Company | Higher based on fleet size |

Factors affecting pricing include:

- Industry risk

- Revenue

- Employee count

- Claims history

- Coverage limits

- Business Location

Insurance companies study risk obsessively

That’s basically their entire business model

Kansas Weather Affects Insurance Heavily

Kansas weather deserves respect

Especially tornado season

Strong storms create billions in property damage across the Midwest over time, and insurers absolutely factor regional weather into pricing

Business in storm-prone areas may see higher premiums for:

- Roof coverage

- Wind damage

- Commercial property insurance

Older buildings sometimes cost more to insure too

Repair expenses increase when structures age poorly

Industries in Kansas needing Strong Insurance

Some industries carry higher risk automatically

Construction Companies

Contractors deal with:

- Employee injuries

- Equipment theft

- Property damage claims

- Vehicle accidents

Construction insurance costs usually run higher because risk exposure stays constant

Agriculture Businesses

Kansas agriculture remains huge

Farm operations often need:

- Equipment coverage

- Crop insurance

- Liability protection

- Commercial vehicle insurance

Farm machinery alone can cost hundreds of thousands of dollars

One severe storm or fire creates massive losses quickly

Trucking and Transportation

Kansas sits near major transportation routes

That means trucking companies remain active statewide

Commercial trucking insurance becomes expensive because accident claims involving large trucks can become catastrophic financially

Insurance companies know this Very well

Restaurants and Food Businessses

Restaurants face constant risks:

- Kitchen fires

- Food contamination

- Customer injuries

- Employee accidents

Insurance becomes essential because restaurants already operate on tight profit margins in many cases

One uninsured disaster can shut businesses down permanently.

Why Small Businesses Skip Insurance Sometimes

Usually money

Owners try cutting costs early

Some assume:

‘Nothing bad will happen’

Then reality appears aggressively

A lawsuit doesn’t care whether a business recently opened or has thin profit margins

Insurance feels unnecessary until disaster arrives

Then suddenly it becomes the smartest expense a business owner ever purchased.

How to Choose the Right Business Insurance in Kansas

The cheapest policy isn’t automatically the best choice

Coverage matters more than bargain pricing

Understand Your Risks

A graphic designer has different risks than an HVAC contractor

Buy coverage matching actual operations

Sounds obvious

People still ignore this constantly

Compare Deductibles Carefully

Lower premiums sometimes mean much higher deductibles

That creates problems during claims

A business saving small monthly amounts may suddenly owe thousands during an emergency.

Always check deductible amounts carefully before signing policies.

Review Exclusions

Policies don’t cover everything

Flood damage, cyber incidents, or employee theft may require additional protection depending on policy details.

Read exclusions closely

Or have an insurance professional explain them clearly

Insurance language loves hiding painful surprises deep inside boring paragraphs.

Business Insurance Claims in Kansas

Claims processes vary by insurer

Usually businesses must:

- Report incidents quickly

- Document damages

- Submit evidence

- Work with adjusters

Photos help massively during property claims

So does organized recordkeeping

Messy documentation slows everything down.

Common Mistakes Kansas Business Owners Make

Underinsuring Property

Construction and replacement costs increased heavily over recent years.

Old coverage limits may no longer fully replace damaged buildings or equipment

That creates major financial gaps after disasters.

Ignoring Cyber Threats

Even tiny businesses store customer information now

Email Systems

Payment Records

Employee Files

Hackers target weak systems constantly.

Failing to Update Policies

Businesses evolve

Revenue changes

Employees increase

Equipment gets added

Coverage should evolve too.

Outdated policies create dangerous blind spots.

Buying Coverage without Comparing Companies

Insurance pricing varies heavily between providers

Shopping around matters

One company may aggressively price restaurant coverage while another heavily increases rates for the same business category.

Best Kansas Cities for Small Business Growth

Several Kansas cities continue supporting strong small business activity

Wichita

Manufacturing, aviation, healthcare, and construction drive major business activity here.

Commercial insurance demand stays strong because of industrial operations and growing service businesses

Overland Park

This area attracts professional services, healthcare businesses, and technology companies.

Professional liability and cyber coverage grew heavily in this market

Kansas City, Kansas

Transportation and logistics business remain active due to regional shipping routes.

Commercial auto and trucking insurance matter heavily here.

Topeka

Governement – related businesses, healthcare providers, and retail companies remain important parts of the local economy.

Small business growth continues steadily

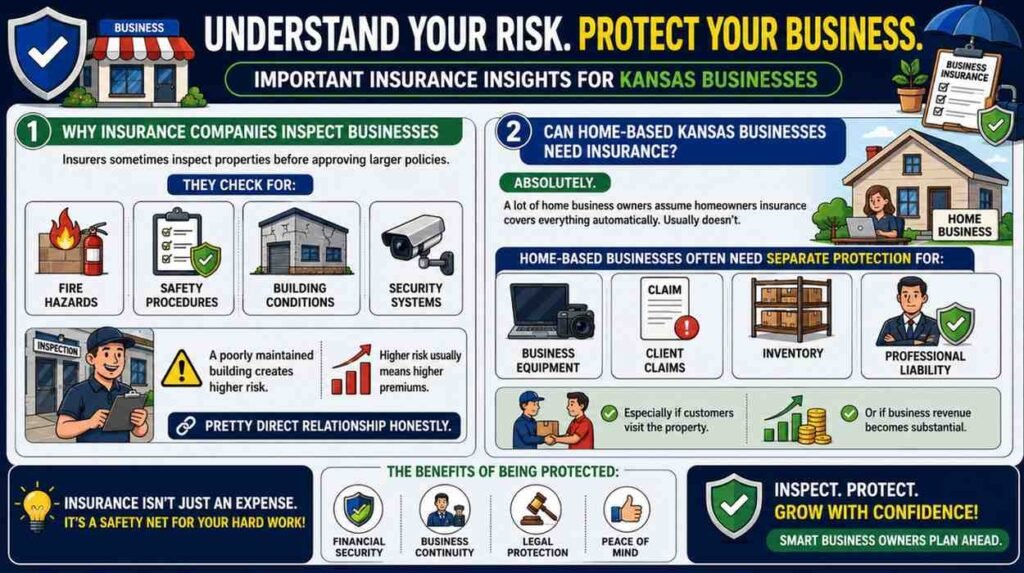

Why Insurance Companies Inspect Businesses

Insurers sometimes inspect properties before approving larger policies

They check for :

- Fire hazards

- Safety procedures

- Building conditions

- Security systems

A poorly maintained building creates higher risk.

Higher risk usually means higher premiums

Pretty direct relationship honestly.

Can Home-based Kansas Businesses need Insurance ?

Absolutely

A lot of home business owners assume homeowners insurance covers everything automatically

Usually doesn’t

Home-based businesses often need seperate protection for:

- Business Equipment

- Client Claims

- Inventory

- Professional Liability

Especially if customers visit the property

Or if business revenue becomes substantial.

Online Businesses in Kansas still need coverage

Digital Businesses face risk too

Ecommerce stores

Marketing agencies

Freelancers

Counsultants

Problems Include:

- Copyright Claims

- Data Breaches

- Contract Disputes

- Client Lawsuits

Online businesses sometimes underestimate legal exposure because operations feel less physical.

Lawsuits still happen online constantly.

Business Insurance Kansas Trends for 2026

A few patterns continue shaping the market

Higher Property Insurance Costs

Storm-related losses keep pressuring rates upward across parts of the Midwest.

Kansas businesses already noticed premium increases.

Cyber Coverage Demand Rising

More small businesses now buy cyber policies after seeing ransomware attacks hit companies nationwide

Awareness increased dramatically.

Bundled Policies Growing

Business owners want simpler insurance management.

Bundled packages continue gaining popularity because handling 9 separate policies feels exhausting.

And Confusing.

And slightly capable of causing stress-induced eye twitching after reading enough insurance documents.

Business Insurance Kansas Coverage Matters More Than People Think

A lot of owners view insurance as an annoying bill.

Until something breaks

Or burns

Or crashes

Or floods

Or ends up inside a lawsuit.

Then coverage suddenly becomes the thing keeping the business alive.

Kansas businesses deal with real operational risks every day. Weather alone creates enough uncertainty to justify strong protection for many industries.

And honestly, businesses that survive long term usually plan for bad scenarios before those scenarios happen.

That’s part of staying in business.

Not Exciting.

Still Important.

For More Updates Please Follow Click Here