How to Lower the Interest Rate on My Credit Card (Proven Ways to Save Money Fast)

Introduction :

Why Your Credit Card Interest Rate Matters Morethan You Think :

If you’ve ever looked at your credit card statement and felt a little shock seeing how much interest you’re paying, you’re not alone. For many people, the interest rate – often called the APR (Annual Percentage Rate) – quietly eats away at their finances month after month.

Here’s the truth : Your credit card interest rate is not always fixed. Many people assume it’s set in stone, but in reality, there are several smart, practical ways to reduce it – some instantly, others over time.

Lowering your interest rate can :

- Save your thousands of rupees (or dollars) over time

- Help you pay off debt faster

- Reduce financial stress

- Improve you overall financial health.

In this Guide, i’ll walk you through proven, real world strategies – no fluff, no theory – that people actually use to successfully reduce their credit card interest rates.

Understanding Credit Card Interest : The Basics Made Simple :

Before lowering your rate, you need to understand how it works

What is APR ?

APR (Annual Percentage Rate) is the yearly interest charged on your outstanding balance. Most Credit Cards have :

- Purchase APR (for regular spending)

- Cash Advance APR (usually higher)

- Penalty APR (applied if you miss payments)

Why is Your APR is So High ?

Your Interest Rate depends on :

- Your Credit Score

- Your Payment history

- Your income and financial stability

- Market conditions (linked to central bank rates)

In India, typically credi card interest rates range between 30%-48% annually. Which is extremely high compared to loans.

Step 1 : Call Your Credit Card Issuer (Yes, It Works More Than You Think)

This is the simplest – and most underrated – strategy.

How it Works

Bank don’t want to lose good customers, if you’ve been paying on time, they may reduce your rate your rate just to keep you.

What to Say

When You call Customer Care :

- Be polite but confident

- Mention your good payment history

- Ask Directly : is there any way you can lower my interest rate ?

Pro Tip :

If they hesitate, say :

- You’ve received better offers from other banks

- You’ve considering switching cards

Real Insight

Many users report reductions of 3%-10% just by making a call. It takes 10 minutes but can save you thousands.

Step 2 : Improve Youtr Credit Score (The Longterm Game Changer)

Your credit score is the biggest factor in determining your interest rate.

Why It Matters

A higher credit score signals lower risk to lenders, which means :

- Better interest rates

- Higher credit limits

- More negotiation power

How to Improve It

- Pay bills on time (no exemptions)

- Keep credit utilization below 30%

- Avoid multiple loan applications

- Maintain older accounts

Example

Let’s say :

- Score : 650 – APR : 42%

- Score : 750 – APR : 30%

That difference can cut your interest by nearly 25% overall

Step 3 : Transfer Your Balance to a Lower Card

Balance transfer is one of the smartest moves if you already have debt.

What is Balance Trasfer ?

You move your outstanding balance to another credit card with :

- Lower interest rate

- Or 0% introductory APR for a limited time

Benefits

- Immediate reduction in interest

- Easier debt repayment

- Temporary relief from high charges

Things to Watch

- Processing fee (usually 1%-3%)

- Limited 0% period (6-12 months)

- Reversion to higher APR later

Best Use Case

If you’re serious about clearing debt quickly, this strategy is powerful

Step 4 : Negotiate Using Competing Offers

Banks are competitive – they don’t want to lose you

How to Use This

- Check offers from another credit cards

- Look for lower APR deals

- Use them as leverage

What to Say

I’ve received an offer with a lower interest rate. Can you match or beat it ?

Reality Check

Even if they don’t match it fully, they often :

- Reduce your APR

- Offer temporary relief

- Give promotional rates

Step 5 : Convert Your Outstanding Balance into EMI

This is a common option in India and works well for large balances

How It Works

Instead of paying revolving interest, your balance is converted into :

- Fixed monthly installments

- Lower interest rate

Benefits

- Predictable payments

- Lower effective interest

- Faster debt repayment

Example

Instead of paying 36% annual interest. EMI conversion might reduce it to 12%-18%

Step 6 : Pay More Than the Minimum Amount

This may sound basic, but it’s incredibly powerful

The Problem with Minimum Payments

If you only pay the minimum :

- Interest keeps compunding

- Debt lasts for years

Better Approach

- Pay as much as you can above minimum

- Target high interest balances first

Strategy Tip

Use the ”Avalanche Method”

- Pay off the highest interest card first

- Then move to the next

Step 7 : Ask for a Temporary Hardship Program

If you’re facing financial difficulty, don’t stay silent

What Bank Offer

- Reduced interest rates

- Waived late fees

- Flexible payment plans

When to Use This

- Job loss

- Medical emergency

- Temporary income drop

Important

This won’t hut your relationship with the bank – in fact, it often helps

Step 8 : Avoid Late Payments at All Costs

Late Payments can trigger a penalty APR, which is much higher

What Happens

- Your rate can jump to 45%+

- It may stay that way for months

Solution

- Set autopay for minimum amount

- Use reminders

- Pay before due date

Consistency builds trust – and better offers

Step 9 : Upgrade or Switch to a Better Card

Sometimes, your current card is just not competitive anymore

Look for Cards That Offer

- Lower APR

- introductory offers

- Rewards + Low interest combo

When to Switch

- Your score has improved

- You’ve outgrown your current card

- You’re paying high interest unnecessarily

Step 10 : Reduce Credit Utilization Ratio

This is one of the most overlooked factors:

What Is It ?

The percentage of your credit limit you’re using

Ideal Range

- Below 30% is good

- Below 10% is excellent

How It Helps

Lower utilization

- Improves your credit score

- Strangthens your negotiation power

Real Life Example : How One Smart Move Saved Thousands

Ravi had :

- 100000 credit card debt

- 36% interest rate

He :

- Called his bank – reduced to 30%

- Transferred balance – 12% EMi

Result

- Interest reduced by more than 60%

- Debt cleared faster

- Monthly stress reduced significantly

This isn’t rare – it’s achievable

Common Mistakes to Avoid

- Ignoring your interest rate completely

- Only paying the minimum

- Taking multiple cards without a plan

- Missing due rates

- Not negotiating with your bank

These mistakes keep you trapped in high interest cycles

Expert Insights : What Actually Works Best

After years of observing real financial behaviour, heres what works :

- Calling your bank is the fastest win

- Balance trransfer is the most powerful short term solution

- Credit score improvement is the best long term startegy

Most people don’t try these – not because they don’t work, but because they don’t know.

Advanced Strategies to Lower Credit Card Interest Rate (That Most People Don’t Know About)

If you’ve already tired the basic methods and still feel like your interest rate is too high, this is where things get interesting. There are deeper, more strategic approaches – used by financilly savvy individuals – that can make a significant difference over time.

Leverage Your Relationship With the Bank

Banks don’t just look at your credit card – they look at your entire relationship

Why This Matters

If you have :

- A savings account

- Fixed deposits

- Salary account

- Loans with good repayment history

You already have leverage

What You Can Do

Contact your bank and highlight :

- Your long term relationship

- Your financial stability

- Your consistent transactions

Ask them to review your profile holistically, not just your credit card usage

Insider Insight

Costumers with multiple products often receive preferential interest rates, even if their credit score isn’t perfect

Time Your Request Strategicaly

Most people randomly call their bank asking for a lower interest rate. Timing actually matters more than you think

Best Times to Ask

- After 6-12 months of consistent payments

- After a salary increase

- When your credit score improves

- During festive seasons (banks push offers)

Why Timing Works

Banks periodically review accounts. If you approach them during a positive financial phase, your chances increase dramatically.

Use Pre Approved Offers Smartly

You’ve probably seen messages like :

- Pre approved loan at 12%

- Exclusive credit card upgrade

Most people ignore these. That’s a mistake

How to Use Them

Instead of taking the offer directly :

- Use it as negotiation power

- Show the bank you qualify for lower rates

Example

If your bank offers a personal loan at 12% why should your credit crad be 36% ?

That question alone can trigger a rate review

Split Your Debt Across Multiple Options

This may sound counterintuitive, but sometimes spreading your debt can reduce your overall interest burden.

How It Works

Instead of keeping 2,00,000 on one high interest card :

- Move part to a lower rate card

- Convert some into EMI

- Pay off a portion aggressively

Result

You reduce the average interest rate across your total debt.

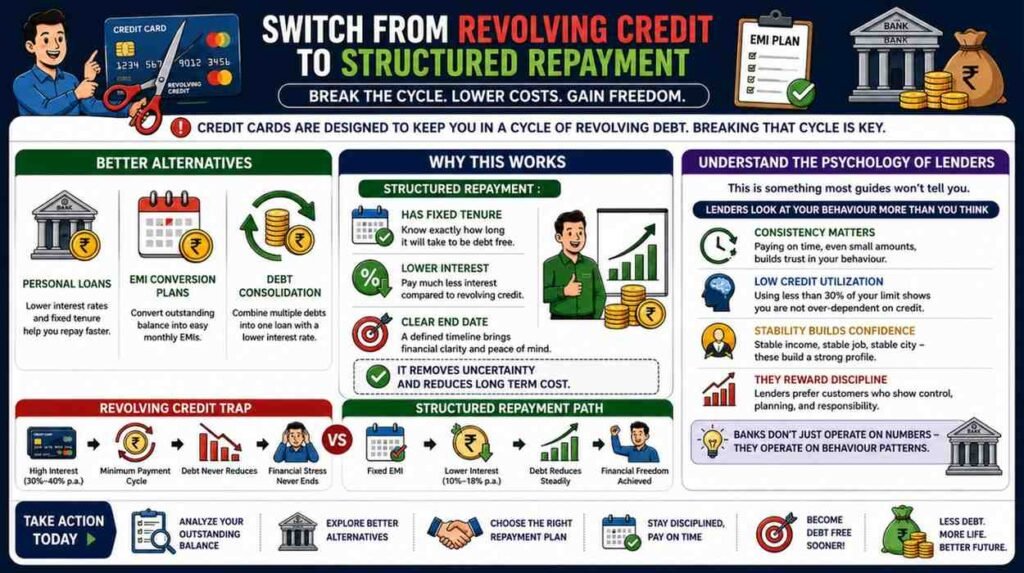

Switch From Revolving Credit to Structured Repayment

Credit cards are designed to keep you in a cycle of revolving debt. Breaking that cycle is key.

Better Alternatives

- Personal loans

- EMI conversion plans

- Debt consolidation

Why This Works

Structured repayment :

- Has fixed tenure

- Lower iinterest

- Clear end date

It removes uncertainity and reduces long term cost.

Understand the Psychology of Lenders

This is something most guides won’t tell you.

Banks don’t just operate on numbers – they operate on behaviour patterns.

What Banks Like

- Predictable customers

- On time payments

- Low risk behaviiour

What Banks Fear

- Losing a good customer

- Default risk

- High maintenance accounts

Your Advantage

If you position yourself as a valuable, low risk customer, banks are more willing to offer better terms.

Create a Personal “interest Reduction Plan’

Instead of random actions, build a simple system.

Step-by-Step Plan

- Check your current APR

- Call your bank and request reduction

- Explore balance trasfer options

- Convert part of debt into EMI

- Increase monthly payment amount

- Track progress every month

Why This Works

Clarity leads to consistency

Consitency leads to results

How Long Does It Take to See Results ?

Let’s be realistic

Immediate Results (1-7 Days)

- Calling your bank

- EMI conversion

- Promotional offers

Short term (1-3 Months)

- Balance transfer impact

- Reduced interest charges

Long Term (3-12 Months)

- Credit Score Improvement

- Permanent lower APR

This is not an overnight fix – but it’s absolutely achievable

The Hidden Cost of Doing Nothing

Let’s put things into perspective

If you have :

- 1,50,000 blance

- 36% annual interest

You could end up paying 50,000 + in interest alone over time.

Doing nothing is actually the most expensive decision

Smart Habits That Keep Your Interest Low Forever

Once you lower your interest rate, the next goal is to keep it that way.

Build These Habits

- Always pay before due date

- Avoid maxing out your card

- Review statements monthly

- Limit unnecesssary spending

- Use credit cards as a tool, not support

Frequently Asked Questions (FAQs)

- Can I really negotiate my credit card interest rate ?

Yes, absolutely. Many banks are open to negotiation, especially if you have a good payment history and a decent credit score. A simple call can sometimes lead to a reduction.

2. How much can my interest rate be reduced ?

It depends on your profile, but typically reductions range between 2% to 10%. In some cases, promotional or EMI plans can reduce it even more.

3. Will asking for a lower interest rate affect my credit score ?

No, requesting a lower interest rate does not impact your credit score. It’s considered a normal customer service request.

4. Is balance transfer a good option for everyone ?

It’s best for people who already have high outstanding balances and want temporary relief from high interest. However, you must repay within the low interst period to maximize benefits.

5. What is the fastest way to reduce credit card interest ?

The quickest methods are :

- Calling your bank

- Converting your balance into EMi

- Using a balance transfer

These can show results almost immediately

6. Can I reduce interest without paying off my full balance ?

Yes, Options like EMI conversion and negotiation allow you to lower interest even if you still carry a balance.

7. What hapens if I miss a payment ?

Missing a payment can increase your interest rate significantly due to penalty APR. It can also damage your credi score.

8. Should I close my credit card to avoid high interest ?

Not necessarily. Closing a card can impact your credit score. It’s better to manage it wisely and reduce the interest rate instead.

9. Does a higher salary help in lowering interest rates ?

Yes, indirectly, a higher income improves your financial profile, making banks more willing to offer better terms.

10. Can I lower interest on multiple credit cards at once ?

Yes, you can apply the same strategies – negotiation, balance transfer, EMI conversion – to each card indivdually

Final Thoughts :

Lowering your credit card interest rate is not about luck – it’s about awareness and action.

Most people continue paying high interest simply because they don;t realize they have options. But once you understand the system and start using the right strategies, everything changes.

You don’t need to be a financial expert.

You just need to take the first step.

And that step could be as simple as picking up your phone and asking the right question.

For More Updates Please Follow Click Here