In House Financing – Complete Guide to Benefits, Risks, and How It Works

Introduction : Why In House Financing is Gaining Popularity

Imagine you’re standing ina a car dearlership, eyeing that perfect SUV you’ve been dreaming about for months. Your credit score isn’t stellar, banks have turned you down, but the salesperson smile and says, ‘No problem – we offer in house financing right here – ‘Suddenly, driving off the lot feels possible.

Traditional lenders like banks and NBFCs have strict rules – credit score requirements, income proof, documentation, and approval delays. This is where in house financing steps in as a powerful alternative. In house financing lets sellers act as their own lenders, cutting out banks and making big purchases accessible to more people.

Over the last decade, especially in markets like India and the U.S. In house financing has grown rapidly. Small businesses, car dealerships, real estate developers, and even medical service providers are offering it. As of 2026, with rising interest rates from traditional lenders and economic shifts, more businesses are embracing it to boost sales. But here’s the truth : In house financing can either be a smart financial move – or a costly mistake – depending on how well you understand it.

What is In House Financing ?

At its core, in house financing (also called seller financing or captive financing) happens when a business or individual provides a loan directly to the buyer for a purchase, bypassing third party banks or finance companies.

The Seller becomes the lender for their own products

Let’s simplify with an example :

- You want to buy a car worth 8 lakhs

- The bank rejects your loan application

- The dealership says : ‘No problem, we’ll finance it ourselves’

- You pay a down payment + monthly installments directly to them

This direct credit line from seller to buyer often comes with customized terms like lower down payments or lenient credit checks, making it a lifeline for those with thin credit files or self employed incomes.

Key Features of In House Financing

Understanding these will help you evaluate any offer :

- Faster Approval

- Flexible Terms

- Minimal Paperwork

- Higher Interest Rates (in most cases)

- Direct Negotiation Possible

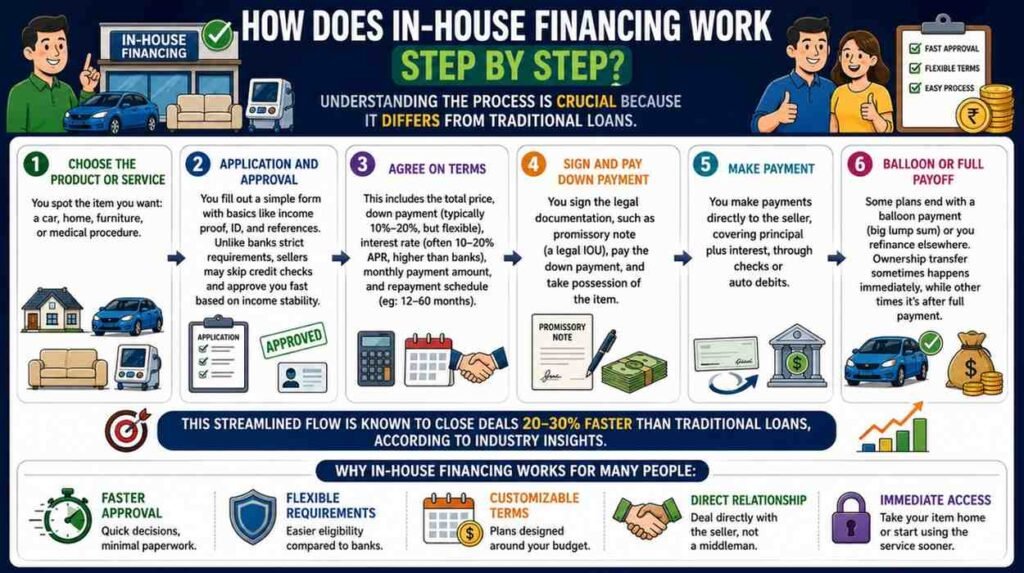

How Does In House Financing Work Step by Step ?

Unerstanding the process is crucal beause it differs from traditional loans

- Choose the Product or Service : You spot the item you want : a car, home, furniture, or medical procedure.

- Application and Approval : You fill out a simple form with basics like income proof, ID, and references. Unlike banks strict requirements, sellers may skip credit checks and approve you fast based on income stability.

- Agree on Terms : This includes the total price, down payment (typically 10%-20%, but flexible), interest rate (often 10-20% APR, higher than banks), monthly payment amount, and repayment schedule (eg : 12-60 months)

- Sign and Pay Down Payment : You sign the legal documentation, such as promissory note (a legal IOU), pay the down payment, and take possession of the item.

- Make Payment : You make payments directly to the seller, covering principal plus interest, through checks or auto debits.

- Balloon or Full Payoff : Some plans end with a balloon payment (big lump sum) or you refinance elsewhere. Ownership transfer sometimes happens immediately, while other times it’s after full payment.

This streamlined flow is known to close deals 20-30% faster than traditional loans, according to industry insights.

Types of In House Financing Across Industries

- Car Dealership Financing (‘Buy-Here-Pay-Here’) : Very common, especially for used cars. Dealerships approve buyers based on income rather than credit score.

- Real Estate Seller Financing : Common for rural properties or off market deals. Buyers pay sellers monthly with 10-30% down, ideal when banks decline

- Retail Store Financing (EMI) : Stores offerig EMI plans for electronics, appliances, and furniture let you buy now and pay later over 6-24 months. These are often advertised as ‘no-cost EMI.

- Medical Financing : Hospitals and dental clinics may offer payment plans for emergency or high cost treatments, boosting service uptake.

- Small Business/B2B Financing : Equipment makers or local businesses may offer installment options to other businesses.

Benefits of In House Financing for Buyers

- Easy Approval (#1 Benefit) : Ideal for people with low credit scores, no credit history, self employed individuals or those rejected byy banks.

- Faster Process : Same day approval and immediate purchase, unlike the days or weeks banks can take

- Flexible Terms : You can directly negotiate the down payment, EMI amount, and loan duration

- Convenience : The entire process of selection, financing, and documentation happens in one place.

- Good for Urgent Needs : Useful for medical emergencies or immediate necessary purchases.

Benefit for Sellers and Businesses

- Close More Deals : Say yes to 20-50% more customers that banks reject, significantly boosting sales volumes.

- Earn Intereset Profits : Capture interest profits that would otherwise go to bank.

- Build Customer Loyalty : Financed Buyers are more likely to return for service, upgrades, or future purchases

- Higher Margins : No bank fees eat into profits.

- Faster Inventory Turnover : Goods are sold and moved faster, smoothing cash flow over time.

Drawbacks and Risks for Buyers

- Higher Interest Rates : Sellers take a higher risk, so they charge higher rates, sometimes 2times more than bank rates (eg : 12-20% APR)

- Hidden Charges : Processing fees, late payment penalties, and documentation charges can be common

- Limited Legal Protection : Banks are highly regulated; in house financing providers may not follow strict rules or include unfair clauses.

- Risk of Swift Repossession : If you miss payments, the seller can repossess the asset quickly, with no foreclosure delays.

- Limited Credit Building : Not all sellers report payments to credit bureaus, meaning your on time payments may not improve your credit score.

Risks for Sellers Offering In House Financing

- Full Default Risk :Your bear the entire loss if the buyer defaults, unlike with a bank loan.

- Cash Flow Constraints : Sales revenue comes in monthly installments rather than a lump sum, straining liquidity.

- Collections Burden : Managing collections and dealing with delinquencies can be a headache.

- Compliance Obligations : Relevant licensing and fair lending laws may still apply.

In House Financing vs Traditional Bank Financing

This Comparison highlights the key differences :

| Aspect | In House Financing | Traditional Bank Loan |

| Approval Speed | Hours to Days | Weeks |

| Credit Requirements | Flexible, Bad Credit OK | Strict, High Score Needed |

| Interest Rates | Higher (10-20% APR) | Lower (5-10% APR) |

| Down Payment | 10-20% Negotiable | 20-30% Fixed |

| Terms | 1-5 Years Typically | Up to 30 Years |

| Repossession | Fast, Direct by Seller | Legal Process, Slower |

| Protections | Fewer Regulations | Strong Consumer Laws |

| Documentation | Minimal | Extensive |

Banks win on rates and protections : in house wins on access and speed.

Real – World Examples and India Insights

- Examples : Ford Credit finances over 40% of Ford Sales. BHPH dealerships like Owings Auto Specialize in subprime used car financing. In India, developers like Camella and Primal Finance offer in house options for homes, with rates of 12-16% for faster closes compared to bank rates.

- In India 2026 : In house financing is common in real estate (especially with PMAY schemes), cars and retail. It fills gaps where bans can’t provide loans, and Budget 2026 is expected to boost all forms of financing.

Smart Tips for Using In House Financing Safely

- Always Compare Interest Rates : Don’t accept the first offer. Compare with banks, NBFCs and credit cards.

- Read the Agreement Carefully : Look for hidden charges, penalty clauses and ownership terms.

- Negotiate Everything : Interest rate, down payment, EMI amount, and loan duration are all negotiable.

- Avoid Long Tenures : A longer tenure means you pay more in total interest.

- Calculate Total Cost : Focus on the total payment over the loan’s life, not just the monthly EMI

- Verify Seller Reputation : Choose to work only with trusted, reputable sellers.

Legal and Tax Considerations

- Legal : Promissory notes are essential. Ensure written agreements are in place with a clear payment schedule and ownership clarity. Record liens for assets where applicable.

- Taxes : Sellers must report interest as income. Homebuyers may be able to deduct home interest under relevant tax codes. Consult a professional to avoid gift tax issues on unrecorded loans.

Expert Insight

After observing financial behavior for years, one pattern is clear :

People don’t fail because of financing – they fail because of poor decisions

In house financing is not inherently good or bad. It’s a tool.

Used Correctly : It helps you grow and solves urgent problems

Used Poorly : It creates debt traps.

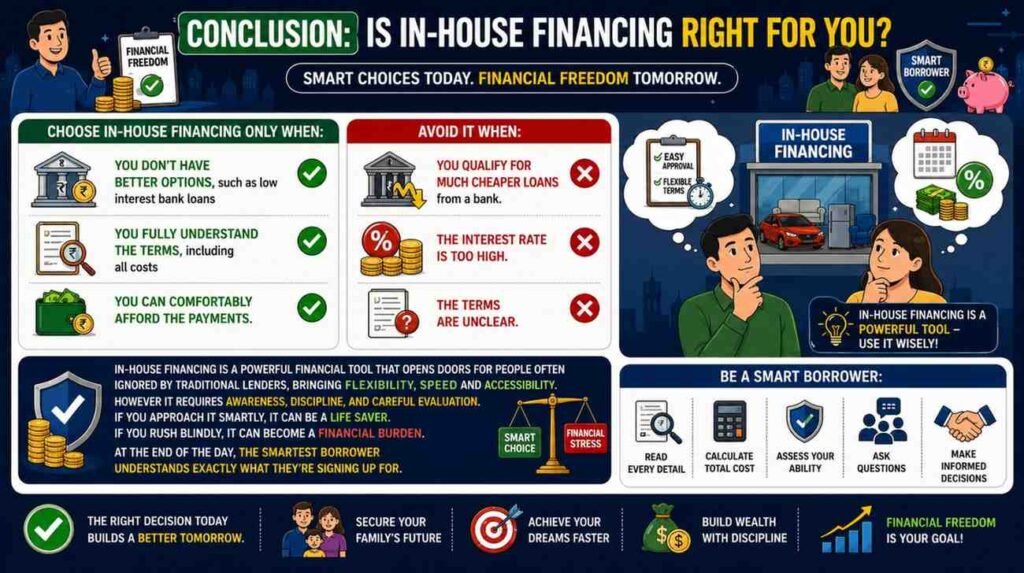

Conclusion : Is In House Financing Right for You ?

Choose in house financing only when :

- You don’t have better options, such as low interest bank loans

- You fully understand the terms, including all costs

- You can comfortably afford the payments

Avoid it When :

- You qualify for much cheaper loans from a bank

- The interest rate is too high.

- The terms are unclear

Inhouse financing is a powerful financial tool that opens doors for people often ignored by traditional lenders, bringing flexibility, speed and accessibility. However it requires awareness, discipline, and careful evaluation. If you approach it smartly, it can be a life saver. If you rush blindly, it can become a financial burden. At the end of the day, the smartest borrower understands exactly what they’re signing up for.

In House Financing FAQs (Frequently Asked Questions)

- What is in house financing ?

In house financing is when a seller or business directly provides a loan to the buyer for a purchase, skipping traditional banks. The buyer makes monthly payments to the seller.

2. How does in house financing work ?

Buyers apply on site, get approved fast based on basic income proof, negotiable terms, sign a promissory note, and make monthly payments directly to the seller. Possession often happens same day

3. Is in house financing a good option ?

Yes, for people with low credit scores or lack of documentation who cannot qualify for traditional bank loans. However interest rates and terms must be checked carefully

4. What are the main advantages ?

Key perks include speedy approvals (hours vs weeks), lenient credit checks, customizable terms, no prepayment penalties, minimal documentation, and convenience.

5. What are the main disadvantages ?

Main disadvantages include higher interest rates (10-20% APR or more), hidden charges, fewer consumer protections, and quick repossession on default.

6. Is in house financing better than bank financing ?

It excels in speed and accessibility but lags in lower rates and strong protections. Banks are better for strong credit buyers.

7. Can you get in house financing for cars ?

Yes, ‘ But-here-pay-here’ (BHPH) dealerships specialize in it, especially for used cars.

8. Is it available for real estate ?

Absolutely, known as owner or seller financing, common for off market or rural properties

9. What about furniture or appliances ?

Retailers offer widespread EMI plans for home goods, acting as a form of in house financing.

10. How common is it in India ?

Very common in real estate, cars, and retail, with CAGR of mortgage market growing.

11. Are there tax implications ?

Sellers report interest as income. Homebuyers may deduct interest under certain codes. Proper promissory notes help avoid gift taxes – consult a tax expert.

12. What credit score do you need ?

There is no strict minimum. Approvals focus more on down payment and income stability than credit score.

13. Can you pay off early ?

Usually yes, often with no penalties, saving on interest. Always check the contract.

14. What happens if you default ?

Sellers can repossess assets quickly as they hold the lien. Communication is key to negotiate.

15. Is it safe and legitimate ?

Yes, from reputable sellers with clear contracts. Verify reviews and ensure legal documents are filed.

16. Why do sellers offer it ?

Sellers offer it to increase sales, attract more customers, and earn additional income through interest.

17. How to choose the best deal ?

Compare interest rates, check the total repayment amount, read all terms carefully, avoid hidden charges, and choose a trusted seller.

For More Updates Please Follow Click Here